24 / 52

24 / 52

23

Any diffusion, publication or exploitation requires to cite the source: International Observatory of

Management Control - DFCG – Decision Performance Conseil

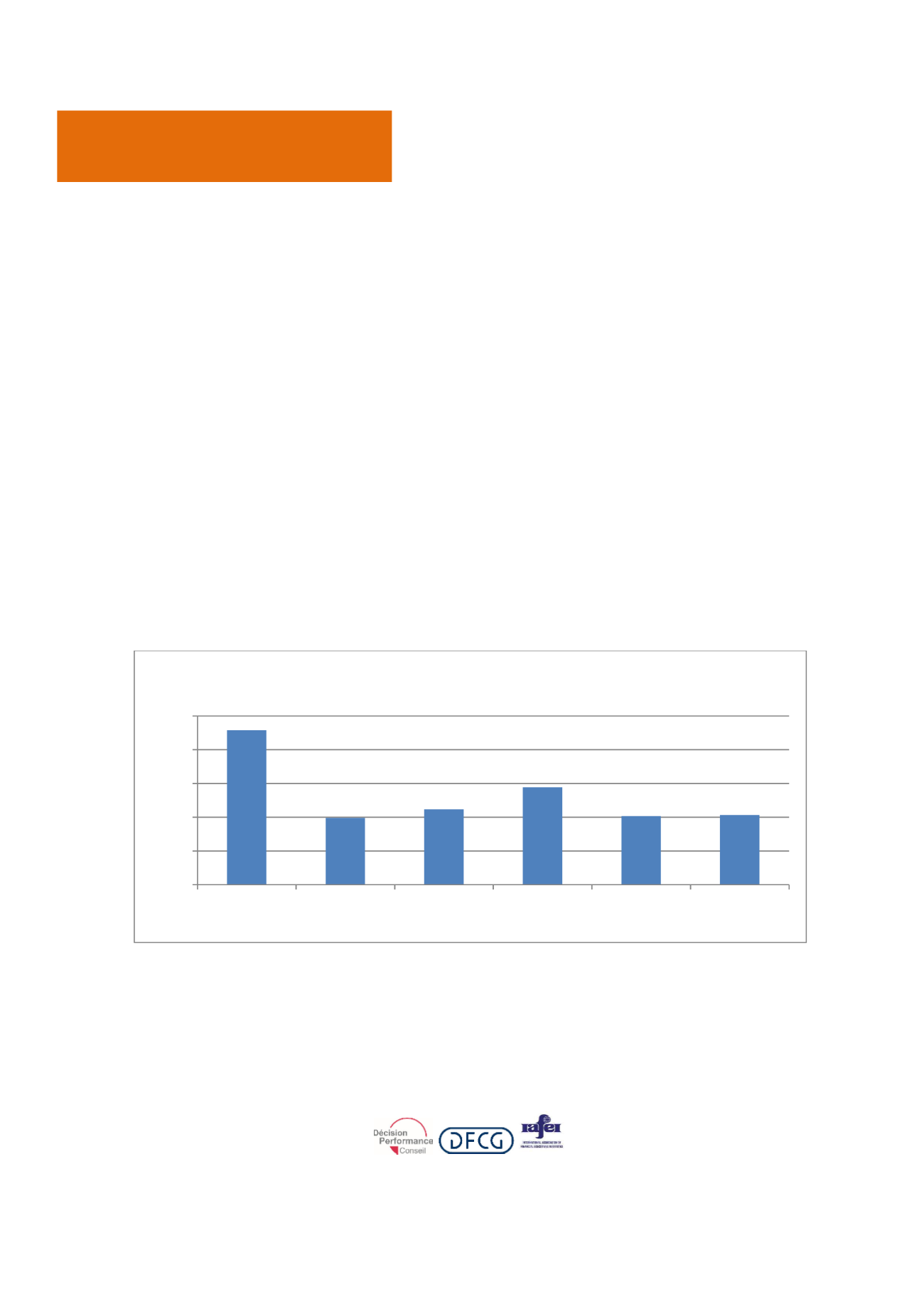

In line with the previous year approach, we asked Financial Directors about methods used for

their Management Control. We selected the following methods:

•

Benchmark: we can compare the company’s performance with those of similar companies

•

Balanced scoreboard: in an uncertain environment, prospective dashboards may

anticipate predictable evolution. They track the company’s performance beyond pure

financial performance.

•

Activity Based Costing/Activity Based Management: as a result of the increasing portion

of indirect cost in total cost, we have recourse to alternative cost allocation method. The

ABC/ABM method is a solution for improving the understanding of

creation cost

mechanisms

.

•

Zero Based Budget: under this method, the baseline is not automatically approved year

after year. Every expense must be justified. We focus on those expenses creating value.

BENCHMARK REMAINS PREDOMINANT, THE BBZ IS PROGRESSING SLOWLY, THE BSC IS

MAINLY EMPLOYED BY LARGE ORGANIZATIONS

Observations carried out during the previous IOMC reports remain unchanged: Benchmark is still

the preferred method for putting into perspective the company's performance. The overall rate

of utilization of the Benchmark method (when combining internal and external approach)

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

Internal

benchmark

ABC ABM Balanced

Scorecard

External

benchmark

ZBB

Other

% of use

METHODOLOGY

IAFEI Quarterly | 23