22 / 40

22 / 40

52% OF RESPONDENTS KEEP THE SAME

INDICATORS FOR THEIR REPORTING

Fig. 16 Contribution of operational staff to budgeting

Regarding the financial indicators used in the budget, 60% of companies establish a balance sheet and a cash flow

statement in addition to P&L, which entails a slight increase compared with 2014 (+5 pts).

͞We speŶd oŶe ŵoŶth to Đlose the ďudget, iŶĐludiŶg ŵeetiŶgs with

the operational staff, followed by a week dedicated

to data consolidation. We are currently leading a project for a common budget tool.

͟

Sabine Schmitt

, Management Control Manager, Burkett

–

Germany

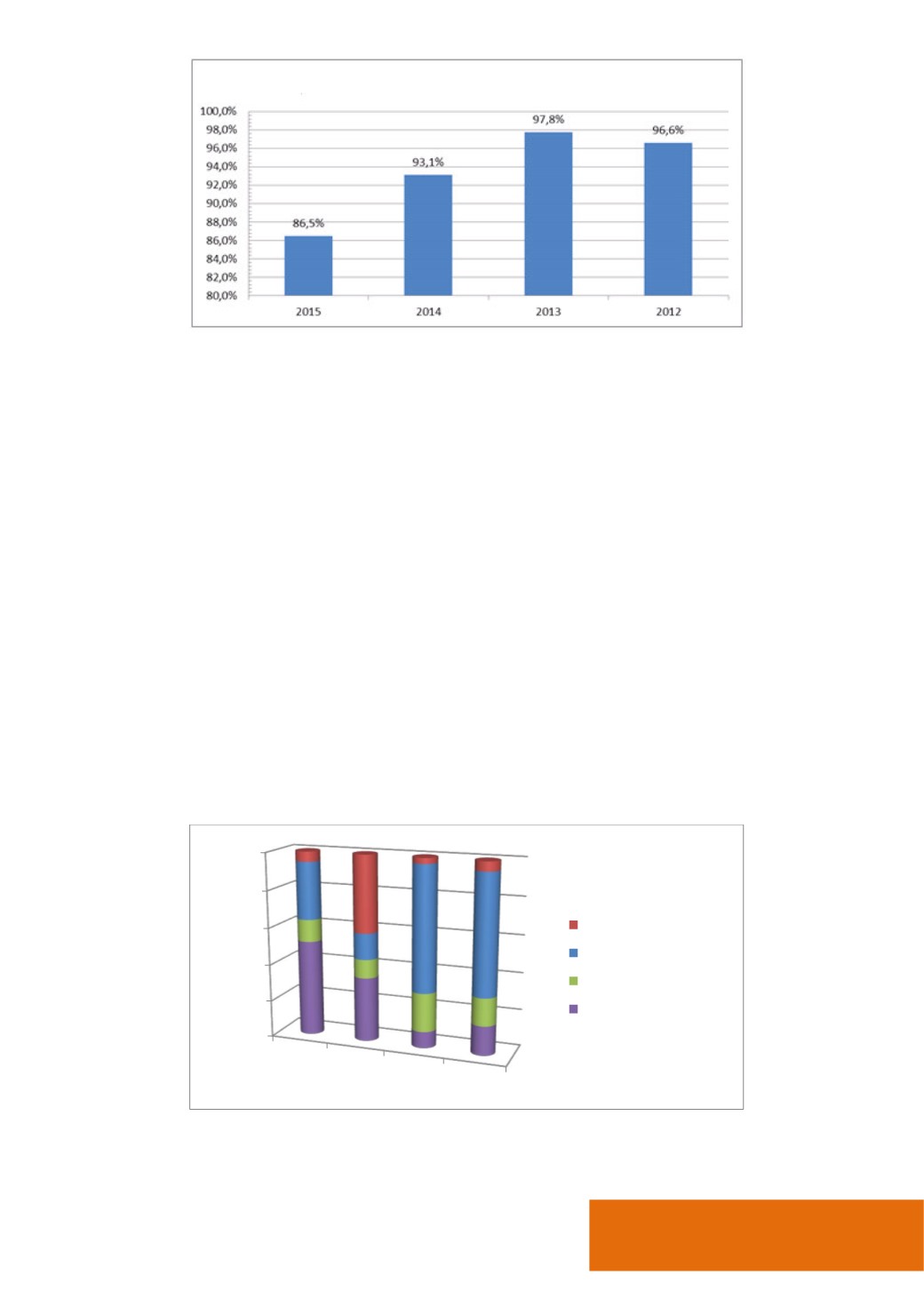

Reporting content is stable

For 52% of the respondents, the number of indicators in the reporting remain the same as the previous year. We find

an increase in the number of indicators for 31% of respondents vs. 14% in 2014, particularly in France (37% of

respondents). We also note that the high-growth companies (revenue growth> 10%) are more likely to increase the

content of their reporting (nearly 41% of respondents).

In contrast, only 5% of respondents have deleted indicators in their reporting, vs. 41% in 2014, which was a year of

stabilization after increasing the number of indicators for 2 years.

Fig. 17 Reporting content over the years

0%

20%

40%

60%

80%

100%

2015

2014

2013

2012

Suppressed indicators

Additional indicators

Indicators replacement

Unchanged

IAFEI Quarterly | Special Issue | 21